Jan

6

The Impact of Proposed Disclosure Requirements for Small Business Loans

The Impact of Proposed Disclosure Requirements for Small Business Loans

Financing options for small businesses will likely decline in 2023 due to the expected passage of new disclosure requirements by Federal and State authorities.

In 2021, the Consumer Financial Protection Bureau (CFPB) proposed rules to expand consumer-like loan requirements to small business financing.[i] Representative Velazquez (D-NY) subsequently introduced H.R. 6054 – the Small Business Disclosure Act of 2021, extending the CFPB’s authority to regulate small business financing like the Bureau’s oversight of consumer lending.

Several states, notably California[ii] and New York,[iii] passed laws in 2022 requiring lenders to disclose

- the total amount of funds provided,

- the total dollar cost of financing,

- term or estimated term,

- method, frequency, and amounts of payment,

- a description of prepayment penalties, and

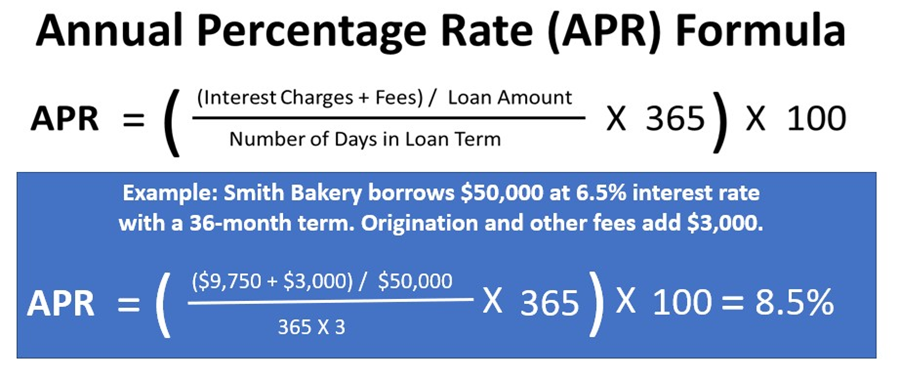

- the total cost of the financing expressed as an annual percentage rate (APR) (until January 1, 2024).

Seven other states[iv] - Connecticut, Missouri, New Jersey, North Carolina, Virginia, Utah, and Maryland – have introduced legislation requiring similar disclosures but are unlikely to be in force before 2023. Nevertheless, small business lenders will likely be subject to more aggressive disclosure laws.

APR Calculation Limitations

The 1968 Truth in Lending Act required disclosure of the APR in nearly all consumer credit transactions.[v] When the loan amount, fees, interest rate, and term are established at the transaction’s initiation, translating the cost of a loan to an annual percentage rate (APR) is simple.

However, an APR calculation is misleading for funding options with indeterminate repayment amounts and terms, such as merchant cash advances, invoice factoring, and short-term loans.

In such cases, lenders set the repayment amount by multiplying the cash advance by a Factor rate of 1.1 to 1.5 based on the lender’s perspective of the repayment risk. The repayment structure benefits small business owners by varying the amount and number of individual payments. The infusion of working capital is short-term, typically repaid in months rather than years.

A blanket requirement to provide an APR calculation would be impossible for these funding types. The most likely result is that lenders offering such funding products will discontinue such products in states where APR disclosure is required.

APR Confusion

Using the APR for transactions with variable interest rates, payment periods, or interim fees complicates the calculation and can produce misleading results. Numerous studies suggest that consumers with APR disclosures continue to misunderstand the data and choose more expensive options.[vii],[viii]

Small business borrowers are unlikely to better understand APR than consumers. A 2020 study by the Kingsley-Kleinman Group for the Small Business Finance Association (SBFA)found that APR disclosures are more likely to confuse potential borrowers than help them make decisions.

Consequences of an APR Requirement

Financial lending transparency is as American as apple pie and Old Glory. Few lenders or borrowers dispute the importance of valid information and full disclosure of lending conditions in plainly written, easily understood language. The Small Business Finance Association (SBFA) advocates Best Practices – Small Business Finance Association (sbfassociation.org) to ensure borrowers understand all aspects of the loan transaction.

According to Paul Kupiec of the American Enterprise Association, non-bank finance companies are critical for small businesses. Their innovation and willingness to accept risk provide financing and services that banks have abandoned. The line between banks and non-bank lenders will effectively disappear if the proposed regulations are passed in their present form, specifically the requirement to include the disclosure of an Annual Percentage Rate (APR) for all commercial loans.[ix]

Applying APR requirements to small business short-term financings will eliminate funding options, drive up borrowing costs, and make it harder for small businesses to receive funding when needed.

Final Thoughts

The banking industry advocates for stronger regulations of non-bank lenders for competitive reasons, not concerns that non-bank lenders exploit small business owners. Small business owners choose non-bank lenders for their faster decision process, lower collateral requirements, and more flexible product terms than bank lenders.

Small business owners will likely contend with a difficult financing environment in 2023 and 2024 from the combination of higher interest rates due to the Federal Reserve’s rate increases. Higher interest rates affect small businesses to a greater degree because they lack the tools and flexibility of larger companies.[x] The loss of funding options like merchant cash advances and other short-term financing solutions makes survival more difficult.

________________________

[i] Staff. (2021) CFPB Proposes Rule to Shine New Light on Small Businesses’ Access to Credit. Consumer Financial Protection Bureau News Release. (September 1, 2020) CFPB Proposes Rule to Shine New Light on Small Businesses’ Access to Credit | Consumer Financial Protection Bureau (consumerfinance.gov)

[ii] Staff. (2022) DFPI’s Commercial Financing Disclosure Regulations Approved to Become Effective as of December 9, 2022. California Department of Financial Protection & Innovation Press Release. (June 14, 2022) DFPI’s Commercial Financing Disclosure Regulations Approved to Become Effective as of December 9, 2022. | The Department of Financial Protection and Innovation (ca.gov)

[iii] Staff. (2021) ACTING SUPERINTENDENT OF FINANCIAL SERVICES ADRIENNE A. HARRIS ANNOUNCES NEW PROPOSED REGULATION PROMOTING TRANSPARENCY IN LENDING TO SMALL BUSINESSES. New York State Department of Financial Services Press Release. (September 21,2021) Press Release – September 21, 2021: Acting Superintendent of Financial Services Adrienne A. Harris Announces New Proposed Regulation Promoting Transparency in Lending to Small Businesses | Department of Financial Services (ny.gov)

[iv] Sadler, J. & Belfort, G. (2022) Update on state small business commercial financing disclosure laws. Consumer Finance Monitor, Ballard Spahr LLP. (February 16, 2022) Update on state small business commercial financing disclosure laws | Consumer Finance Monitor

[v] Staff. (2015) Truth in Lending Act. Consumer Financial Protection Bureau, pp.14-22. (April 2015) 201503_cfpb_truth-in-lending-act.pdf (consumerfinance.gov)

[vi] Prosser, M. (2015) Why do small business lenders avoid talking about APR? Forbes magazine. (June 22, 2015) https://www.forbes.com/sites/marcprosser/2015/06/22/why-do-small-business-lenders-avoid-talking-about-apr/?sh=6aeae39b10db

[vii] Soll, J. B., Keeney, R. L., & Larrick, R. P. (2013). Consumer Misunderstanding of Credit Card Use, Payments, and Debt: Causes and Solutions. Journal of Public Policy & Marketing, 32(1), 66–81. http://www.jstor.org/stable/43305554

[viii] Mckenzie, C.R., & Liersch, M.J. (2011). Misunderstanding Savings Growth: Implications for Retirement Savings Behavior. Journal of Marketing Research, 48, S1 – S13. Misunderstanding Savings Growth: Implications for Retirement Savings Behavior – Craig R.M. Mckenzie, Michael J. Liersch, 2011 (sagepub.com)

[ix] Kupiec, P. (2021) Putting bank regulations on non-bank lenders will stifle innovation. The Hill. (May 7, 2021) Putting bank regulations on non-bank lenders will stifle innovation | The Hill

[x] Lauria, P. (2022) Interest Rate Increases: 4 Concerns for Small Businesses. Business News Daily. (Downloaded January 2, 2023) How Interest Rate Hikes Impact Small Businesses (businessnewsdaily.com)