Nov

15

Merchant Cash Advances

Merchant Cash Advances – a Small Business Lifeline

Small business owners quickly learn the importance of cash flow to a business. The realization that the money needed to make the next month’s operating expenses is tied-up in accounts receivable – cash you’re owed but haven’t collected – is sobering. The lag between sales and collection becomes critical with growing sales and customers who delay payment. According to the U.S. Small Business Administration, the #1 reason small businesses close is the lack of cash flow.

Accounts Receivable Financing

Securing accounts receivable financing can be difficult, if not impossible, for most small business owners. Even when successful, funding often requires weeks to accomplish. When cash is secured, the business may be teetering on bankruptcy. The friendly banker advertised on television has little interest in lending to companies with little history, revenues, and assets.

Factoring – The Sale of Accounts Receivable

Unable to get financing from banks and facing a “cash crunch,” business owners often turn to “factoring” – selling their receivables to a third party at a discount. The factor then collects the amount owed by the business customers, sometimes employing aggressive, harassing collection tactics that destroy future relations between the small business and the customer. While factoring is a legitimate form of funding, business owners should carefully choose their factor and understand its collection practices.

Merchant Cash Advances – Alternative to Bank Loans & Factoring

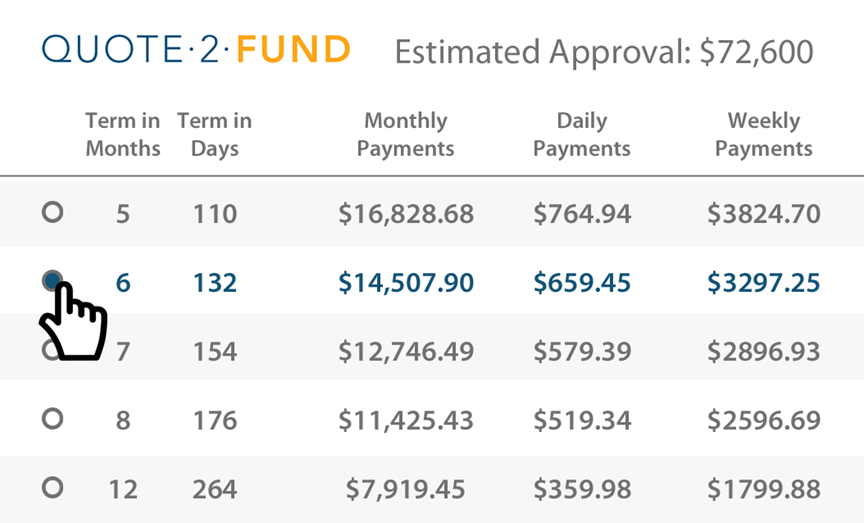

Merchant Cash Advances are a growing alternative of revenue-based finance. The funds are not a loan but an advance payment of future sales. Repayment occurs through automatic deductions of a percentage of credit card sales or regular bank account withdrawals.

The repayment period typically ranges from three to eighteen months. The amount repaid (110% -140% of the advance) is based on the company’s industry, history, and financials, including the average amounts and trends of credit card transactions.

Unlike a typical loan, the total fees are fixed at the time of the advance, while the repayment term depends on the level of credit card receipts. A growing business with increasing credit card amounts will pay off the advance more quickly than a business with level growth.

Small business owners are attracted to merchant cash advances because

- Easy Application Process. Applying for a bank loan or negotiating a factoring agreement can take weeks to complete. Online applications with minimal documentation are typical with merchant cash advances, approvals usually occurring within 24 hours following receipt of the application.

- Rapid Cash Funding. Once approved, funds are deposited directly into the company’s designated bank accounts, typically by the next business day after approval.

- Flexible Approval Requirements. Companies with bad credit or limited histories generally have few financing opportunities. Merchant cash advances are based primarily on revenue and credit card transactions, without requirements of physical collateral or interaction with customers of the business.

- Variable Repayment Schedule. Repayment of the cash advance through a fixed percentage of credit card payments ensures that the drain on the company’s cash flow is limited. When revenues rise or fall, the fixed rate never changes.

Merchant cash advances are ideal for companies with significant credit card transactions that need fast access to cash.